Fri, 14 July 2017

My guest today is Kevin Erdmann, he blogs about economics and finance at Idiosyncratic Whisk. Kevin has written a ton about housing, as evidenced by the titles of his blog posts. A recent one is labeled Housing: Part 239. This series is part of a larger book project that Kevin is publically drafting on his blog. We discuss the housing bubble of the 2000s and the post-2008 housing market. I took my first undergraduate economics class in 2008, just as the financial crisis was beginning, so there's never been a time in my economics career when people weren't talking about this. And yet, I still have so much to learn! Kevin makes an interesting distinction between "open-access cities" and "closed-access cities." Closed-access cities are places like San Francisco, New York, and San Jose that have restricted their housing supplies. Open-access cities are places like Houston and Phoenix with more elastic housing supplies. We talk about these factors and how they relate to the housing boom and bust, liquidity, and central bank policy. Kevin points out that supply side restrictions on housing construction are necessary for demand-side factors to cause housing bubbles. That's because in a market with an elastic housing supply, more demand doesn't result in higher prices, it just causes more homes to be built. Related links: Credit supply, housing supply, and financial crises

|

Fri, 7 July 2017

The guest for this episode is Jonathan Morduch, he is a professor of public policy and economics at NYU and the author of The Financial Diaries: How American Families Cope in a World of Uncertainty, co-authored with Rachel Schneider. The book looks at the financial situations of ordinary American families. It is centered around a detailed survey of 235 households where they recorded what they earned and what they spent at an extremely granular level. From a truck mechanic whose income depends on bad weather wearing out the parts on trucks to a blackjack dealer whose tips literally depend on her customers' winnings at the blackjack table, the surveys reveal a huge amount of variance in the incomes and expenses of these households. This variance is not captured in annualized statistics, but it has profound implications for the way these households spend and save. We discuss financial literacy in the context of the real problems people face and relate the stories to some results from behavioural and experimental economics.

|

Fri, 30 June 2017

In this episode, I have three guests on the show with me: Kewei Hou of Ohio State University, Chen Xue of the University of Cincinnati, and Lu Zhang of Ohio State University. Kewei, Chen, and Lu have coauthored a paper titled "Replicating Anomalies," a large-scale replication study that re-tests hundreds of so-called "anomalies" in financial markets. An anomaly is a predictable pattern in stock returns, or stated differently, it is a deviation from the efficient markets hypothesis. Their abstract reads as follows: The anomalies literature is infested with widespread p-hacking. We replicate the entire anomalies literature in finance and accounting by compiling a largest-to-date data library that contains 447 anomaly variables. With microcaps alleviated via New York Stock Exchange breakpoints and value-weighted returns, 286 anomalies (64%) including 95 out of 102 liquidity variables (93%) are insignificant at the conventional 5% level. Imposing the cutoff t-value of three raises the number of insignificance to 380 (85%). Even for the 161 significant anomalies, their magnitudes are often much lower than originally reported. Out of the 161, the q-factor model leaves 115 alphas insignificant (150 with t < 3). In all, capital markets are more efficient than previously recognized. We discuss the process of replicating these anomalies, issues involving the use of equal-weighted vs value-weighted returns, and the problems of p-hacking in finance research. Works Cited Hamermesh, Daniel S. 2007. “Replication in Economics.” Canadian Journal of Economics 40(3):715–733. Other Links The Marginal Revolution post on this paper.

|

Fri, 16 June 2017

My guest on this episode is Kevin B. Grier of the University of Oklahoma. Our topic for today is a paper Kevin wrote on the economic consequences of Hugo Chavez along with coauthor Norman Maynard. I had Francisco Toro on the show last year to discuss Venezuela's economic history, so you can listen to that episode if you want a refresher on Chavez. For this episode, our main topic is the empirical method Kevin used to quantify Chavez' effect on Venezuela: synthetic control. Synthetic control is a relatively new empirical technique. It grew out of an older technique called difference in differences (or diff-in-diff). Diff-in-diff is simple and intuitive: Given two statistics with parallel trends, we can compare their changes before and after some intervention affecting only one of them to see the effect of the intervention. So for instance, if you wanted to know the effect of Seattle's minimum wage increase, you could compare the employment trend among low-skilled workers in Seattle to the same trend in Portland. Then assuming Seattle and Portland would have had similar trends if not for the minimum wage hike, we say the difference between the employment growth in the two cities is attributable to the minimum wage hike. But what if Seattle and Portland don't have similar trends? What if there's no labour market similar enough to Seattle's to provide a valid comparison? That's where synthetic control comes in. Seattle might not be like Portland, but it might be like a weighted average of Portland, San Francisco, and several counties just outside Seattle. We could construct this weighted average and call it a synthetic Seattle; it is designed to mimic the dynamics of Seattle's labour market before the minimum wage hike. Then if the synthetic Seattle deviates from the real Seattle after the wage hike, we can attribute that difference to the hike. This is what Kevin has done to study the impact of Hugo Chavez on Venezuela. Listen to the episode to find out his results! |

Fri, 9 June 2017

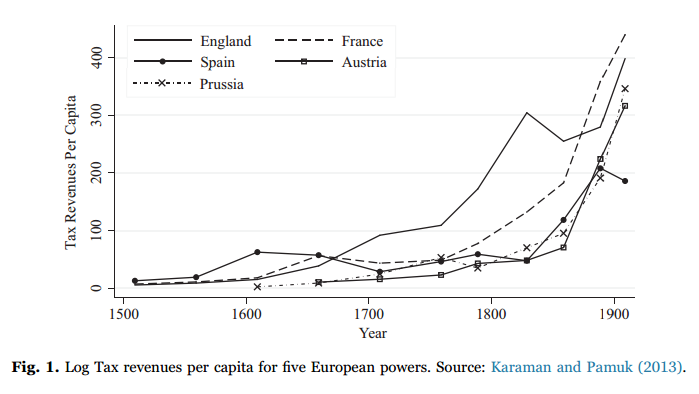

My guest for this episode is Mark Koyama of George Mason University. Our topic is a recent paper titled, "States and Economic Growth: Capacity and Constraints," which Mark coauthored with Noel Johnson.

As stated in the paper, "state capacity describes the ability of a state to collect taxes, enforce law and order, and provide public goods." That said, state capacity does not mean big government. A state may have the power to impose rules across its territory, but it doesn't have to use that power in a tyrannical way. Another way of saying that is to say that having a high state capacity is compatible with Adam Smith's desire for "peace, easy taxes, and a tolerable administration of justice." One metric that researchers use to measure state capacity is tax revenue per capita. But as Mark is careful to point out, a state with less state capacity can still sometimes achieve a relatively high income through tax farming. This is the practice in many pre-modern states of auctioning off the right to extract tax revenues to local elites in different regions. We discuss the rise of modern nation-states in various regions, and why some states developed more state capacity than others going into the twentieth century. In particular, we discuss Europe's transition away from a feudal system ruled in a decentralized way by monarchs who held power based on their personal relationships with local lords. England's Glorious Revolution of 1688 allowed it to develop its state capacity earlier than other European nations, with a centralized tax system controlled by parliament.

By contrast, continental powers like the French Ancien Régime and the Hapsburg Empire were legally and fiscally fragmented, leading them to develop their state capacity much later than England. We also discuss the development of state capacity in Asia, and why Meiji Japan was able to develop its state capacity much faster than Qing Dynasty China.

|

Fri, 2 June 2017

My guest for this episode is Nuno Palma, he is an assistant professor of economics, econometrics, and finance at the University of Groningen. Our discussion begins with the monetary history of England. Nuno has authored a study that reconstructs England's money supply from 1270 to 1870. We discuss his methods and findings. We also discuss the influx of precious metals into European markets after the discovery of the New World. We discuss the impact of empire on economic development with reference to Nuno's work on the Portugese empire. We revisit some topics from my previous interview with Jari Eloranta. Later in the conversation, we discuss the effect of trade on economic growth during the industrial revolution. Nuno places a greater importance on international trade than McCloskey and Mokyr, but a lesser importance than historians like Wallerstein. Although gross trade flows were not particularly large, trade created new domestic industries like the porcelain industry that was created to compete with Chinese imports. Imports also encouraged urbanization among the European population, something that created many positive spillover effects over the long term.

|

Fri, 26 May 2017

My guest for this episode is Jari Eloranta, he is a professor of comparative economic and business history at Appalachian State University. Jari's work focuses on the economic history of national defense. In this far-reaching conversation, we go all the way back to pre-modern societies' methods of financing their militaries, then trace the transitions up through the early modern period and into the 20th century. We discuss the way war has shaped modern states and institutions. Books mentioned: The First Total War: Napoleon's Europe and the Birth of Warfare as We Know It, by David A. Bell. The Gunpowder Age: China, Military Innovation, and the Rise of the West in World History, by Tonio Andrade. |

Sat, 15 April 2017

My guest today is Alex Lubinsky, co-founder of the Silicon Valley startup Rentberry. Rentberry is a platform that lets landlords post units for rent so that tenants can bid on them. Once a landlord posts a vacancy, different potential tenants can make offers and the landlord can select which one to rent to. Importantly, the landlord doesn't have to select the highest bidder. Potential tenants on Rentberry put in their personal characteristics up on the site, so landlords can select for the type of tenants they want. Maybe they're willing to accept a lower rent from a quiet single woman than a family of five with four dogs and six cats. There has been some controversy about the site, stemming from the fact that it leads tenants to bid against one another, potentially pushing up prices. One tenant advocate said, "I think it's incredibly arrogant and incredibly concerning in light of the fact that we have the highest number of homeless families since the Great Depression. For them to do something to increase the rents seems really callous." Vanity Fair said Rentberry would turn rental markets into a Hunger Games-like death match. Alex and I address these criticisms in the episode. The critics are missing one simple element to the story, which is that Rentberry doesn't just cause more tenants to bid on any given listing, driving up the price, it also allows each tenant to bid on more listings, driving down prices by giving each tenant more options. The two forces cancel one another. By only charging a one-time fee of $25 when a lease is signed, Rentberry reduces the costs of applying for vacancies. In some markets, tenants can expect to pay hundreds of dollars in application fees while apartment hunting and Rentberry allows them to avoid those. What Rentberry is really doing is allowing the market to approach equilibrium more rapidly. Preliminary evidence also suggests that Rentberry decreases vacancy rates, since these are lower for landlords using the site than for the country in general. This is equivalent to an increase in the housing supply, which is unambiguously good. Listen to the episode for the full discussion. |

Fri, 7 April 2017

Hello and welcome to the fiftieth episode special of Economics Detective Radio! Today we have Ash Navabi back on the program, but we’re flipping the script: Ash will be interviewing me about the show and about all the things I’ve learned while making it. In this episode, I alienate the political right by discussing the importance of labour mobility and the desirability of open borders. I also alienate the political left by expressing a lukewarm position on climate change. I also discuss my own research plans relating to law and economics. Finally, we discuss literature! Really, if you like Economics Detective Radio, you have to hear this episode.

|

Fri, 24 March 2017

Returning to the podcast is Vincent Geloso of Texas Tech University. Our topic for this episode is anthropometric history, the study of history by means of measuring humans. Doing serious historical research into the distant past is difficult work, because the further you look back in time, the less information you can access. For the 20th century we have wonderful thing like chain-weighted real GDP. Going back further, we have some statistics, lots of surviving physical evidence, and loads of documents and writings. Going further than that, we're left with the odd scrap of thrice-copied surviving manuscripts and second-hand accounts from people who lived centuries after the events they describe. And going even further than that, we have just bones and dilapidated temples with the occasional inscription. Anthropometric history allows us to look into the distant past at what economic historians like Vincent hope might be a good measure of different populations' health and standards of living: their heights. People who have healthy upbringings with lots of access to food tend to be taller than people who don't; that's why modern humans are much taller than they were a thousand or even a hundred years ago. Vincent has contributed to this literature with his latest co-authored paper, The Heights of French-Canadian Convicts, 1780s to 1820s. The abstract reads as follows: This paper uses a novel dataset of heights collected from the records of the Quebec City prison between 1813 and 1847 to survey the French-Canadian population of Quebec—which was then known either as Lower Canada or Canada East. Using a birth-cohort approach with 10 year birth cohorts from the 1780s to the 1820s, we find that French-Canadian prisoners grew shorter over the period. Through the whole sample period, they were short compared to Americans. However, French-Canadians were taller either than their cousins in France or the inhabitants of Latin America (except Argentinians). In addition to extending anthropometric data in Canada to the 1780s, we are able to extend comparisons between the Old and New Worlds as well as comparisons between North America and Latin America. We highlight the key structural economic changes and shocks and discuss their possible impact on the anthropometric data. Listen to the full episode for our fascinating discussion of this branch of historical research, including the so-called "Antebellum puzzle," the anomalous observation that American heights decreased in the years prior to the Civil War even though the economy was apparently growing rapidly. We also discuss the heights of slaves in the American South, who were taller than their white counterparts despite being oppressed as slaves.

|

|

Economics Detective Radio

|

||||||||||||||||||||||||||||||||||||||||||||||||||||